Bye Bye Now: Google Eats Expedia (EXPE)

The pandemic is expected to crush The Web monopoly's latest travel offering poses serious threat to entire travel sector – in particular, Expedia.

War – and now travel, it appears — are hell. Travel is not a well understood market. But to us, Expedia (EXPE) has the most questions to answer. Yes, this is a $11.3 billion business with 80% gross margins, and a cool $1.9 billion in annual net cash flows from operations. And the firm is coming off a bullish period, with bond prices and institutional equity holdings on the rise.

Just ask Thomas Cooke, the poor Englishman who was besieged by a vicious Web and phone shaming wave, after furious travelers confused him with Thomas Cook. That is, the 178-year-old English travel company that stranded 155,000 British passengers back in September. It was the largest British repatriation, since the 350,000 troops were fetched off the beach in Dunkirk in World War II.

Most analysts dismiss Thomas Cook’s failure as the usual story: The stodgy incumbent that could not react to a bright and shiny Digital Age. Analysts pointed out that Thomas Cook took on too many debts; it chose the wrong online partner, MyTravel; and it faced stunning losses of £1.5 billion. And it is absolutely true that Thomas Cook had no answer for ruthless Web disruptors, like AirBnb, easyJet and Ryanair.

However, blaming one company for the deeper woes in the travel sector, misses the deeper dysfunction lurking. Flat is suddenly the new up in Web transport, logistics and vacations. Once-glittering IPOs, like WeWork, Uber, and Lyft, are stalling. Fair, a Softbank-backed car subscription service, laid off 40% of its staff. AirBnb’s once-overlooked deep losses now very much worry investors considering its IPO in early 2020.

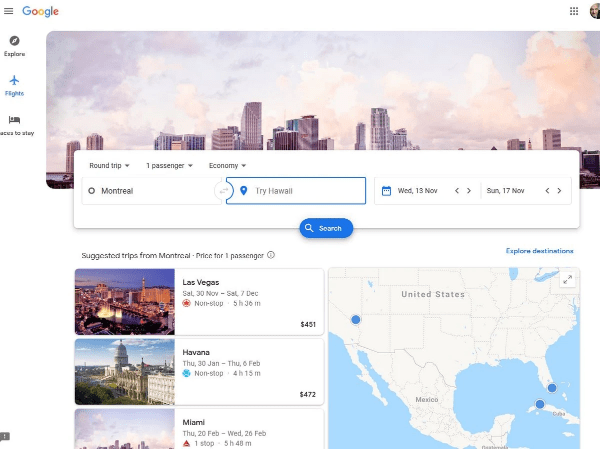

And, most importantly to online travel, back in May, Google quietly rolled out its most sophisticated online travel planning and booking tools to date.

Packaged as Google Explore, Travel and Places To Stay, these integrated Web itinerary, ticketing and lodging services function as a travel version of Google’s massively disruptive Answer Box: That is, the often-framed organic-search results that dominate the upper portion of the left side of the first page of any Google query.

Google Travel works as all things Google does: It efficiently consumes -- oh sorry, curates-- a vast trove of hotel, rental car and lodging data from giants like Booking.com(BKNG), Expedia, and Sabre Group (SABR). Most impressively -- and terrifyingly -- Google then instantly re-targets all that information on Google’s Search and Maps franchises.

Like any good monopolist, Google Travel ruthlessly eats up a sizable chunk of any given travel-search experience. And along with it, an ever-increasing bite of the $2.3 trillion Web and mobile travel planning market.

Similar to deteriorating market conditions in the music industry circa 2001, the news media in 2006 and financial services in 2008, online travel is getting ready for a steep change in altitude,

Time to make sure your seatbelt is fastened and tightly secured around your waist.

Google Travel: Software That Eats Travel

Already, there’s grim news from the front as Google lays siege to the Web travel business. The Australian Financial Review ran a deeply sobering story, back in July, aptly headlined Why Google Will Own Travel. "[Google is] using their popularity as a search engine to decimate competing content providers," complained Stuart McDonald, then owner of Travelfish.org. McDonald said that TravelFish once employed about 20, who serviced about 1.5 million monthly searches. Until, that is, Google rejiggered its search algos, hogged half the traffic and sent Mr. McDonald’s Travelfish to the fillet table.

Margin pressure is also building throughout the Web travel sector. HomeAway, a unit of Expedia, recently got into a spat with its payment processor Yapstone. HomeAway was attempting to collect an extra 6% fee, with whispers of competing with Booking.com’s 15% fees. And, the industry is shifting to an instant-booking model, where travelers and property owners have less control over their inventory.

Google’s travel strategy seems to be part of a larger company policy of referring ever less traffic to outsiders. Jumpshot, a San Francisco-based data provider, published deeply concerning numbers indicating what a closed-shop Google is becoming: Out of 150 billion-plus searches, Jumpshot estimates that a massive 49% of those never leave Google. Of that percentage, 7% is paid search and 6% goes to sites Google also owns. Jumpshot estimate that only 45% of Google’s total search traffic flows out to non-Google owned properties..

Google Travel’s strategy of eating its sector alive is not an anomaly. It is the company’s new mission.

Surviving Google

How professional investors will profit from Google’s takedown of the Web travel sector will vary. There are many players. There are many points of entry. Ask questions.

But then there’s the pricey, 34-times forward price-to-earnings ratios on the stock; and return-on-equity ratios that are 70 percent or so less than the sector averages. But Expedia’s real red flag is its razor-thin profit margins. Bottom line net profits have been stuck down near 3% since 2014.

And then there is the dirty secret of the online travel business: Cash deposits and advances that are terribly tricky to document. Travelers who book online for both tickets and rentals, often pay upfront with significant cash deposits for their reservations. These deposits are for services that might be rendered months, or even years, in the future, when the booked travel actually happens.

These advances and deposits can amount to hundreds of millions of dollars. In Expedia’s case, it books these advances as so-called “Deferred Merchant Bookings” on its statement of operating cash flows. In 2018, these deferred bookings grossed up to be $485 million, or roughly 25% of total operating cash flows. It has always been a point of contention among analysts as to whether these dollars amount to lucrative no-interest loans. Or, are merchant-bookings encumbered assets that are vulnerable to a downturn when travelers cancel plans and request refunds.

Worse, Expedia’s exposure to Web search middlemen, like Google, runs throughout the company. The list of Expedia’s subsidiaries below indicates that essentially all are referral partners of Google. And Expedia’s business units won’t have any other search partner available. Bing!, Google’s biggest competitor, also has a robust Travel page.

Investor’s Proper Web Travel Itinerary

The travel sector won’t be a painless ride for Google. The monopoly has stubbed its toe in the sector before. It’s much vaunted Google Trips app was wound down this past year. Google is not shy about ditching major products like Google Wave, Glass or Google Plus. Google Travel may well be a flop.

But To paraprash Marc Andreessen, co-founder of tech venture-capital investing shop Andressen Horowitz, Web software is eating the world. It’s just in the case of the 21st-century Web travel business, Web software, like Google, is now eating other Web software like Expedia.

It would be prudent for all to avoid being served as the inflight meal on this trip.